Those latest numbers can’t be right….Phoenix is supposed to be one of the worst real estate markets in the country right now with no end in sight.

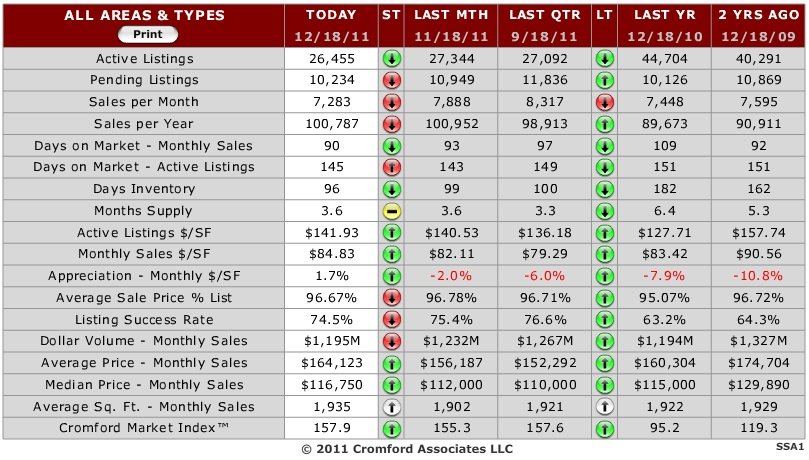

The average price per square foot is now 1.4% higher than it was 12 months ago for Maricopa County as a whole. This is what used to be known as “appreciation”. Yes folks, that’s right, after putting a solid stable base over the last year in pricing, metro Phoenix / Maricopa County is showing a year over year appreciation for both average monthly $/sf ($84.83 2011 from $83.42 2010) and monthly median sale price ($116,000 2011 from $115,000 2010) as of December. Certain micro-markets or some cities and zip codes are still showing depreciation while others show positive appreciation, but on the whole, it looks pretty good.

Only 8,482 new listings were added to ARMLS in the last 30 days. This is 19.5% fewer than the 10,534 added at the same time last year. In fact, we could be facing a pretty significant shortage of homes coming up this next spring buying season and it’s not impossible to see some volatility to high side in pricing as a reaction to this.

With total bank inventory of foreclosed properties (17,800 down to 8,200) , number of homeowners in the process of being foreclosed upon (35,000 down to 18,000), and number of homeowners delinquent on their mortgage to also include those who have already received a foreclosure notice (14% to 7.6%) all seeing about a 50% drop over the last year…the possibility of any sizable shadow inventory of foreclosures flooding our market supply and stalling any recovery in prices is extremely unlikely. While some economists are stating the nation as a whole may be only about halfway through its foreclosure crisis, Mike Orr of the Cromford Report and Tom Ruff of the Information Market project Maricopa county may already have worked our way through 80-90% of the foreclosure tsunami resulting from the real estate boom and bust.

In fact Arizona had the most improved mortgage delinquency rate in the country in the third fiscal quarter 2011.

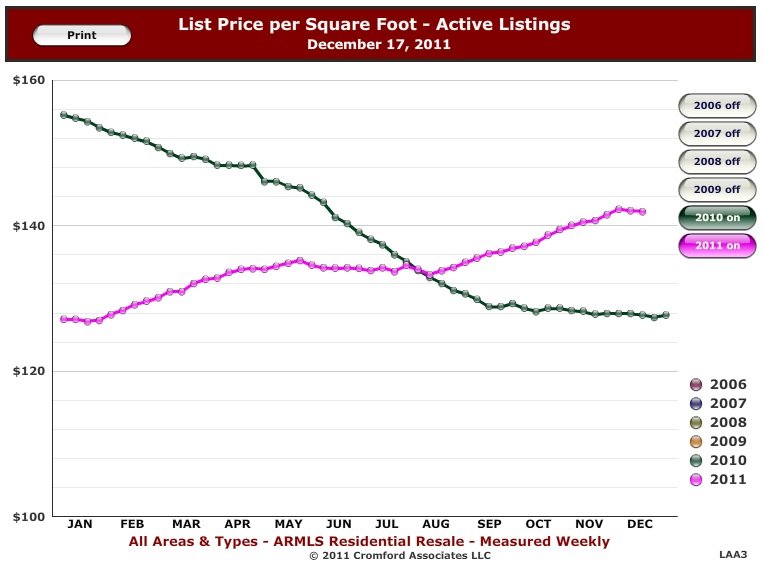

The average list price per sq. ft. for active listings across all areas and types has been moving upwards since mid January. At $140.71 it is now 11% higher than it was 10 months ago and 10% higher than it was this time last year.

No matter how doomsday spinsters try to spin it, we are no longer in a declining market for Phoenix Metropolitan area. To those who have been active in the market either as agents or buyers/sellers they have been getting that feeling for the last several months. The balance of supply and demand has shifted so heavily to a seller’s market for many months now, with supply excessively low and demand remaining strong and steady, that it was only a matter of time before prices started appreciating.

Yes, hard to believe, but it’s not impossible to have appreciating real estate values in a still somewhat sluggish economy and in one of the poster child states for the real estate boom and bust era. Even with the economy not back at full strength, it’s not impossible to have appreciating values. The fundamental laws of supply and demand still apply to some extent, and how the economy is fairing as a whole will only affect how quickly or delayed pricing reacts to that balance. We saw the big shift in market activity heat up at the beginning of this year, and we are now just starting to see prices moving up after being flat for the last 12 months. I’ll post another installment soon on why it can take so long for pricing to respond to market changes. Stay tuned.

Here’s the latest from The Cromford Report for December 2011.

Most of the supply and demand numbers were rather boring in November. All the excitement was concentrated in the pricing action. In this, October and November have been the opposite of the previous 12 months where there were massive changes taking place in supply but not much of interest going on in pricing.

To start with, let us look at the ARMLS data across all areas and types:

-Sales per Month: 7,230 in November – down 5% from October but up 8% from this time last year.

-Active Listings (including AWC): 26,655 on December 1 – down 1.5% from November 1 and down 41% from this time last year.

-Active Listings (excluding AWC): 19,377 on December 1 – down 1% from November 1 and down 50% from this time last year.

-Pending Sales: 10,171 on December 1, down 3% from November 1, but up 2% compared with this time last year.

-Listing Success Rate: 75.3% on December 1 – down slightly from 76.0% on November 1 but up significantly from 60.4% on December 1, 2010.

-Contract Ratio: 90.1 on December 1, down slightly from 91.9 on November 1 but up strongly from 40.1 last year at this time.

-Days Inventory: 96 on December 1, down from 98 on November 1 but dramatically down from 184 at this time last year

-Cromford Market Index™: 155.8 on December 1, the same as on November 1 but far above the 91.0 we saw on December 1, 2010.

-Sales Price as a Percentage of List: 96.67% on December 1, exactly the same as on November 1 but up from 95.59% on December 1, 2010Thus we see evidence of a huge improvement in the market balance compared with December 2010 but little if any change between last month and now. The Cromford Demand Index™ and Cromford Supply Index™ are both flat-lining, meaning that supply remains low and steady and demand remains high and steady.

So let us look at where the action is:

Monthly Average Sales Price per Sq. Ft. – $83.58 in November – up 3.1% over the month before and up 0.9% over last year at this time. It is also up 6.5% compared with the extreme low point measured on September 15

Monthly Median Sales Price – $115,000 in November, up from $112,199 in October and the same as we saw in November 2010.

3.1% in a single month is a pretty strong bounce for $/SF so it is worth looking into exactly how and why this happened. If we look at the details we find:

- Greater Phoenix REOs are up 2.2%

- Greater Phoenix Short sales & Pre-foreclosures are down 4.1%

- Greater Phoenix Normal listings are up 3.1%

So we see that short sales and foreclosures, while booming in sales volume and success, have not been going up in price. In fact they have been falling faster than the other two groups are rising. The gap between the average $/SF for REOs and short sales has never been closer. We also see that overall pricing has improved faster than any of the three groups. This may seem paradoxical at first but the explanation is quite simple. REOs have the cheapest pricing and their sales volume is declining fast due to the reduction in supply. Normal listings are growing market share and have the highest pricing. The change in the mix has a huge effect on the overall average. This is the exact opposite of what happened in 2008 when prices tanked at unprecedented rates.

We can say on balance that sales pricing is back to where it was last year at this time and we can also reasonably expect to see positive appreciation rates for the market as a whole for at least the next 4 months. This is easy to predict because last year we had a gently declining pending listing $/SF whereas now pending $/SF figures are headed upwards.

This positive appreciation is not spread evenly around. The following cities currently show higher prices than at this time last year (measured by average monthly sales $/SF):

- Fountain Hills (14.8%)

- Paradise valley (11.9%)

- Casa Grande (7.6%)

- Sun City (7.1%)

- Buckeye (5.3%)

- Maricopa (3.2%)

- Gold Canyon (2.7%)

- Arizona City (1.9%)

- Phoenix (1.3%)

- Queen Creek / San Tan Valley (1.2%)

- El Mirage (0.8%)

- Cave Creek (0.4%)

The following are still in negative territory:

- Sun Lakes (-14.3%)

- Litchfield Park (-8.5%)

- Goodyear (-7.7%)

- Tolleson (6.8%)

- Avondale (-6.3%)

- Surprise (5.6%)

- Peoria (-5.6%)

- Sun City West (5.3%)

- Mesa (-4.2%)

- Anthem (-4.1%)

- Glendale (-3.8%)

- Apache Junction (-3.4%)

- Laveen (-3.0%)

- Gilbert (-2.8%)

- Chandler (-2.6%)

- Tempe (-0.9%)

- Scottsdale (-0.1%)

Most of the second list are seeing an upward trend in the last two months but are still down compared with November 2010.

For the months of July through October, we saw trustee sales volumes fall while new notices stayed fairly flat. The opposite occurred in November. Foreclosure notice started to fall off again while trustee sales popped up slightly, due to the large batch of Recontrust (Bank of America) notices that were issued in August against Countrywide originated loans. These became ripe for trustees to sell during November. The longer term trend for both is still downward and the pending foreclosure count has started to fall fast again having stabilized for several months. We believe that there will be relatively few REOs generated from now on. Most of the foreclosure tsunami is past us, perhaps 80%. Those foreclosure notice still to come will generate a lot of short sales and third party purchases at the foreclosure auction, but relatively few homes will revert to the beneficiaries. We have probably already seen over 90% of the REOs that are to be created by the 2004-2006 real estate bubble and fewer than 10% are yet to come.