Is Greater Phoenix “Overvalued”?

Mortgage Payments Are Lower Than They Were 13 Years Ago

For Buyers:

Interest rates have been increasing along with the inflation rate as of late, which has spawned a string of headlines about affordability. While the rate hike has knocked some buyers out of the market without a doubt, general affordability hasn’t taken a big hit yet. According to the National Association of Home Builders and Wells Fargo, buyers making the median family income could still afford 65% of what sold in the Valley last quarter. A measure between 60-75% is considered normal.

Let’s look at the historical cost of a 1,900sf home in Greater Phoenix, for example. In March 2005, a home that size would run $281K on average. Today that same home would be $309K, $28,000 more (+10%). However, the interest rate back then was 5.9% compared to 4.5% today, meaning that the principal and interest payment has dropped nearly $100 from where it was 13 years ago for the same home. At the same time, the median family income rose from $58K to $69K according to HUD (+19%). Which is why despite recent increases in interest rates, the affordability of real estate in the Valley is still considered very good.

For Sellers:

Last April CoreLogic released a report ranking the Greater Phoenix area as “overvalued”. In fact, they placed 37% of our nation’s top 100 metropolitan areas in that category. As of May, after 6 years of higher-than-normal appreciation rates, the monthly average sales price per square foot has finally reached its place along the long-term 3% appreciation line established between 2000-2003 before the 2005 bubble and 2008 crash. Meaning that if we had fallen asleep in 2003, and the last 15 years were just a long horrible dream, we would have woken up today and not known anything had happened. Prices are where they would have been had the market followed the average long-term rate of inflation. That brings to light that current appreciation rates of 6% or more are no longer sustainable in the long term. However that doesn’t mean that prices will “peak” or “crash” anytime soon. Most likely as demand slowly wanes, prices will go flat and hang out until they once again fall in line with the rate of inflation, but don’t expect that to happen in 2018. Supply and demand measures today indicate another 3-6 months of positive appreciation for the majority of homes priced below $400K.

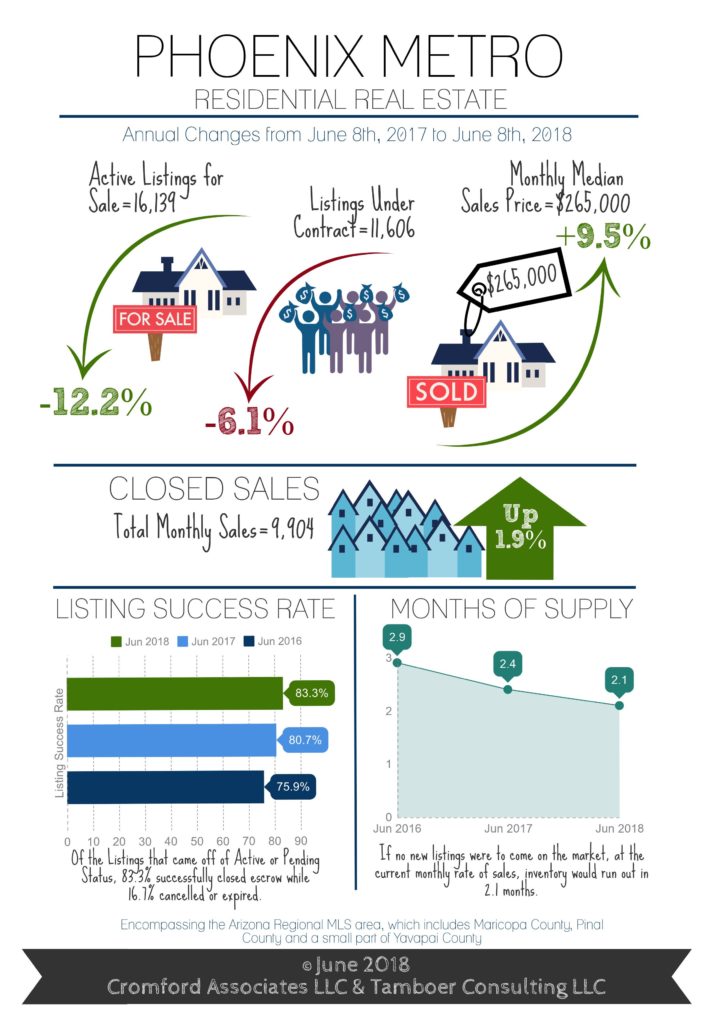

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report