The latest market data for Phoenix from The Cromford Report shows more encouraging news, with inventory down, sales and demand up, foreclosures down, and pricing making the most positive move seen for at least 15 months.

- average active listing $/SF – up 2.3% to $139.98 per sq. ft.

- average pending listing $/SF – up 1.8% to $79.65 per sq. ft.

- average monthly sales $/SF – up 1.1% to $80.95 per sq. ft.

On the surface the preliminary numbers for October suggest it was quite similar to September. Looking at the ARMLS data across all areas and types we see the following:

Sales per Month: 7,556 in October – down 7% from September but up 16% from this time last year.

Active Listings (including AWC): 27,063 on November 1 – up 0.7% from October 1 but down 40% from this time last year.

Active Listings (excluding AWC): 19,578 on November 1 – up 1.3% from October 1 but down 50% from this time last year.

Pending Sales: 10,509 on November 1, down 3% from October 1, but up 9% compared with this time last year.

Listing Success Rate: 75.9% on November 1 – down slightly from 76.2% on October 1 but up significantly from 56.1% on November 1, 2010.

Contract Ratio: 91.9 on November 1, down from 95.1 on October 1 but up from 39.4 last year at this time.

Days Inventory: 98 on November 1, the same as October 1 but dramatically down from 184 at this time last year

Cromford Market Index™: 156.0 on November 1, down from 159.4 on October 1 and 87.9 on November 1, 2010.

Sales Price as a Percentage of List: 96.70% on November 1, almost the same as 96.84% on October 1 but up from 95.21% on November 1, 2010

Just like in October, we can see that all these numbers are far better than 12 months ago but most are not quite as good as the previous month. Supply rose very slightly while demand declined slightly.

However the overall figures hide some spectacular difference between the geographic areas. For example, when it comes to active listings (including AWC), there was little overall change when averaged across all areas and types (up 0.7%), but the following cities increased their supply of single family detached homes far more than average:

- Rio Verde (up 34%)

- Fountain Hills (up 20%)

- Gold Canyon (up 19%)

- Sun City West (up 18%)

- Sun City (up 15%)

- Avondale (up 14%)

- Waddell (up 12%)

- Sun Lakes (up 10%)

- Surprise (up 9%)

- Anthem (up 7%)

- Scottsdale (up 6%)

The following had significant falls in active single family detached listing counts:

- Youngtown (down 5%)

- Queen Creek (down 6%)

- Tempe (down 8%)

- Apache Junction (down 9%)

- Tonopah (down 12%)

- Laveen (down 13%)

We have emphasized many times that changes in the balance of supply versus demand take a long time to be reflected in changes to pricing. This is illustrated by the latest numbers. The supply increased and demand fell during October, yet pricing made the most positive move it has done for at least 15 months, driven by the large reduction in supply over the last 12 months:

- average active listing $/SF – up 2.3% to $139.98 per sq. ft.

- average pending listing $/SF – up 1.8% to $79.65 per sq. ft.

- average monthly sales $/SF – up 1.1% to $80.95 per sq. ft.

Again, the overall average numbers hide discrepancies between different segments of the market. The specific price movements for the different price ranges are:

| Price Range | Oct 2011 Avg $/SF | Sep – Oct 2011 | One Year Change | Lowest $/SF | Lowest Date | Current $/SF Relative to Lowest$/SF |

| Below $100,000 | $44.67 | UP 2.3% | UP 3.0% | $41.63 | Feb 2011 | UP 7.3% |

| Below $25,000 | $20.10 | UP 3.8% | UP 4.7% | $17.92 | Aug 2010 | UP 12.2% |

| $25,000 to $49,999 | $30.36 | DOWN 1.6% | UP 5.4% | $28.07 | Sep 2010 | UP 8.2% |

| $50,000 to $74,999 | $43.59 | UP 3.2% | UP 2.4% | $40.81 | Mar 2011 | UP 6.8% |

| $75,000 to $99,999 | $51.32 | UP 2.5% | UP 1.1% | $48.94 | Dec 2010 | UP 4.9% |

| $100,000 to $124,999 | $60.64 | DOWN 0.9% | DOWN 1.0% | $58.53 | Jan 2011 | UP 3.6% |

| $125,000 to $149,999 | $69.73 | UP 0.2% | UP 1.3% | $66.43 | Jan 2011 | UP 5.0% |

| $150,000 to $174,999 | $76.05 | DOWN 0.3% | UP 2.6% | $74.10 | Oct 2010 | UP 2.6% |

| $175,000 to $199,999 | $82.39 | DOWN 0.8% | DOWN 0.1% | $81.58 | Mar 2011 | UP 1.0% |

| $200,000 to $224,999 | $88.48 | UP 0.8% | UP 1.8% | $85.96 | Feb 2011 | UP 2.9% |

| $225,000 to $249,999 | $92.90 | DOWN 0.5% | DOWN 0.5% | $90.80 | Aug 2011 | UP 2.3% |

| $250,000 to $274,999 | $98.98 | UP 6.2% | UP 4.3% | $95.57 | Jan 2011 | UP 6.7% |

| $275,000 to $299,999 | $101.81 | DOWN 0.9% | DOWN 0.3% | $100.67 | Jun 2011 | UP 1.1% |

| $300,000 to $349,999 | $114.05 | UP 7.4% | UP 8.1% | $101.90 | Feb 2009 | UP 11.9% |

| $350,000 to $399,999 | $116.00 | DOWN 3.2% | DOWN 3.4% | $111.98 | Jan 2009 | UP 3.6% |

| $400,000 to $499,999 | $132.77 | UP 2.9% | UP 4.2% | $126.12 | Mar 2009 | UP 5.3% |

| $500,000 to $599,999 | $149.22 | UP 1.8% | UP 2.1% | $139.66 | Sep 2010 | UP 6.8% |

| $600,000 to $799,999 | $168.75 | UP 1.6% | UP 3.4% | $157.43 | Aug 2010 | UP 7.2% |

| $800,000 to $999,999 | $188.48 | DOWN 7.3% | UP 5.4% | $177.33 | Sep 2010 | UP 6.3% |

| $1,000,000 to $1,499,999 | $241.31 | UP 4.0% | UP 20.4% | $191.18 | Sep 2010 | UP 26.2% |

| $1,500,000 to $1,999,999 | $234.11 | DOWN 6.2% | UP 0.3% | $221.50 | Nov 2010 | UP 5.7% |

| $2,000,000 to $2,999,999 | $326.34 | UP 10.9% | UP 2.5% | $288.90 | Jul 2010 | UP 13.0% |

| $3,000,000 and Above | $385.24 | DOWN 7.3% | UP 10.9% | $347.46 | Oct 2010 | UP 10.9% |

We can see that there were no price ranges hitting new lows last month. Below $150,000 recent pricing tends look healthy and on a strong upward trend. Above this point the picture is rather mixed. All but 5 ranges are showing price appreciation for the last 12 months. So why does the overall market number not show price appreciation? The reason is that the sales volume has decreased in the upper ranges so the more expensive homes make less contribution to the overall mix, driving the overall average down.

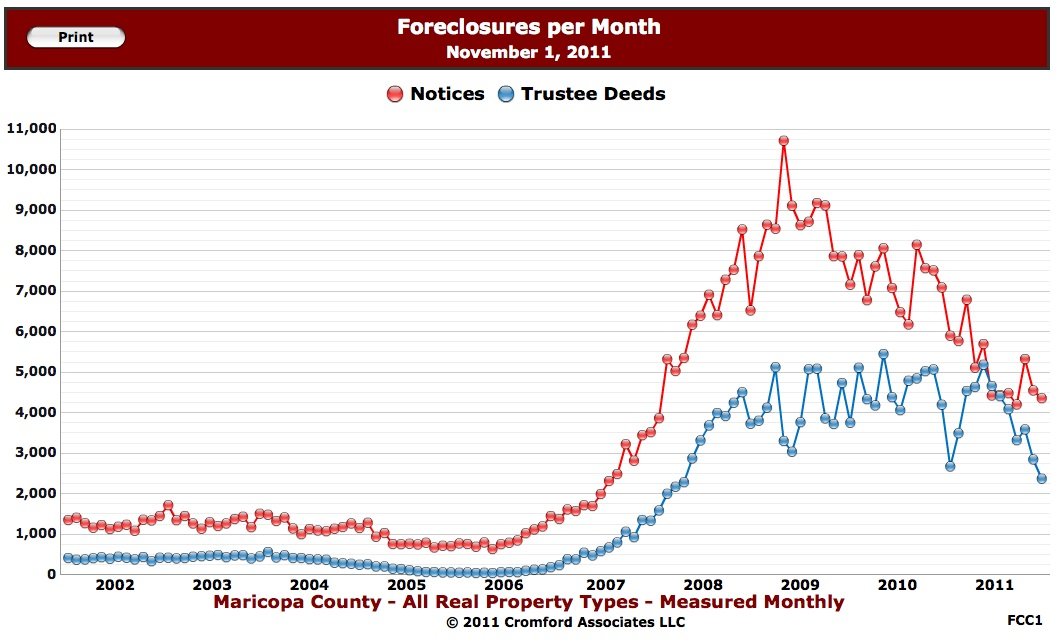

Maricopa County Foreclosures

New notices were down 4% to 4,354 in October. Trustee sales were down 17% to 2,364 the lowest number since March 2008. Sales to third parties were 1,125 leaving only 1,239 going back to the lenders – the lowest total since October 2007.

REO inventory is down to 10,451 almost exactly half of what it was 12 months ago.

This chart tracking completed foreclosures and notices of foreclosure for delinquent homeowners is encouraging, with a strong trend downward, hope it continues…banks can sometimes be no fun to deal with when you’re a home buyer!